Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

Investing in real estate can help you build wealth and achieve financial freedom. Before you take the plunge, it’s essential to understand the current investment property rates available. Knowing what kind of interest rate you can expect to pay on your loan—versus a standard conventional loan—will help determine whether the investment is worth it.

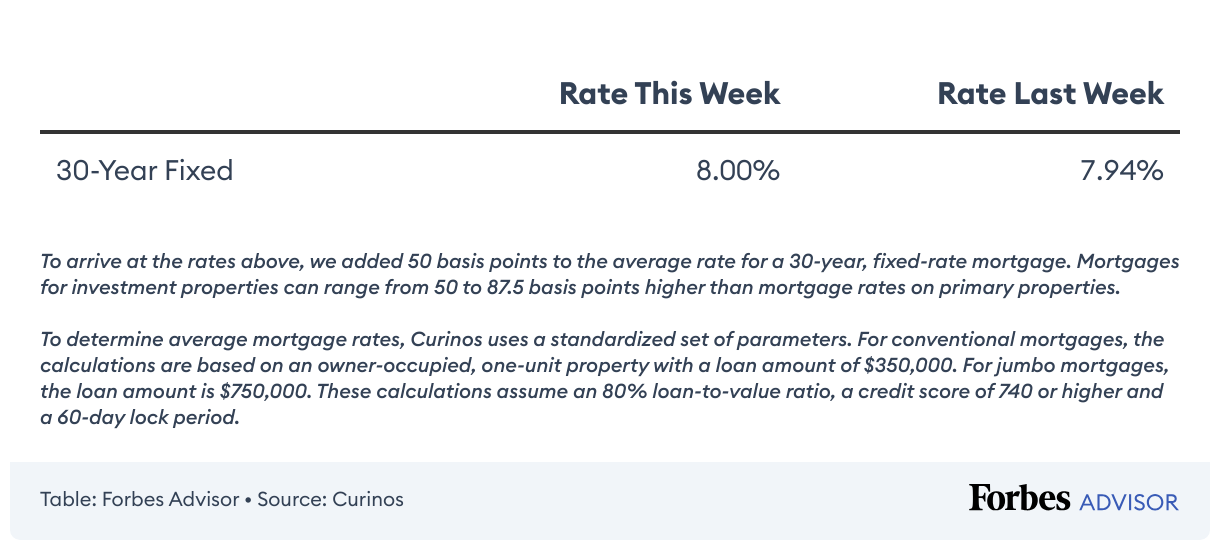

Today’s 30-Year Investment Property Loan Rates

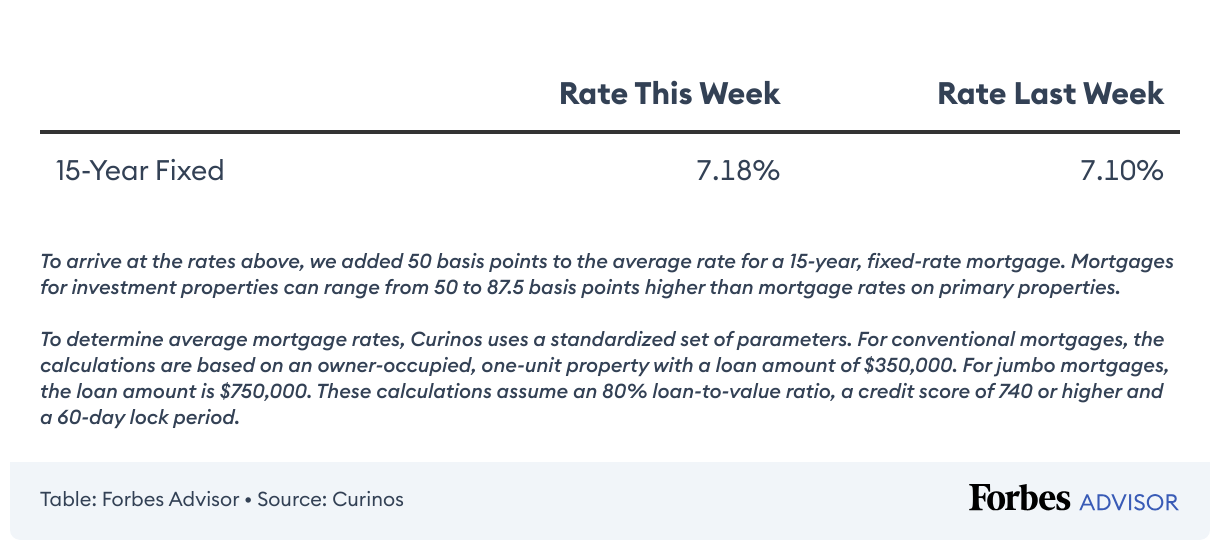

Today’s 15-Year Investment Property Loan Rates

What Are Investment Property Mortgage Rates?

Investment property mortgage rates are the interest charges investors pay to finance a property solely for investment purposes. These rates depend on the investor’s creditworthiness, the cost of the property they wish to acquire and the type of lender they work with. Typically, lenders charge higher interest rates for investment property loans because these properties present more risks than owner-occupied homes. As a real estate investor, paying close attention to interest rates is crucial because they directly impact your cash flow, profitability and the long-term financial viability of your investment portfolio. Knowing where to find the best rates and how to negotiate them effectively can make all the difference in building a lucrative real estate investment portfolio.

How Do Lenders Set Rates for Investment Properties?

Lenders consider several personal and economic factors when setting rates for investment properties. Your credit score is a key determinant, with higher scores often resulting in more favorable rates. Lenders also evaluate your debt-to-income (DTI) ratio—a measure of your total monthly debt payments relative to your monthly income. A lower DTI is typically associated with a better risk profile and can lead to lower rates. The down payment size also matters; larger down payments can significantly reduce the risk for the lender, resulting in lower interest rates. Economic factors beyond the borrower’s control also influence how lenders set rates for investment properties as well. Federal Reserve decisions, such as changes to the fed funds rate, can impact lending rates. Strong economic indicators like robust employment growth and a stable financial market can increase demand for investment properties, potentially driving up rates. Likewise, government policies, such as changes in tax laws or regulations related to investment properties, can also impact rates.

Ways To Finance Investment Properties

Whether residential or commercial, investment properties can be lucrative, but securing financing remains a critical step in the process. The following are some of the common types of financing used for investment properties:

- Conventional loans. Traditional lenders like banks or credit unions offer conventional loans. They usually require a substantial down payment (typically 20% of the property’s value) and a solid credit score—740 or higher will typically get you the most competitive rates.

- Hard money loans. These are short-term loans offered by private lenders, often used by investors who intend to renovate and resell a property quickly. Hard money loans have higher interest rates than conventional loans because they pose more risk to the lender and are typically based on the property’s value rather than the borrower’s creditworthiness.

- Private money loans. Similar to hard money loans, these loans come from private individuals or groups. The terms and rates vary widely, as they’re based on a personal relationship between the borrower and lender. These loans can benefit investors who need funding quickly or cannot qualify for a conventional loan.

- Home equity. This type of loan or line of credit depends on how much home equity you possess—that is, the difference between what you owe on your home and its current market value. Home equity loans offer competitive interest rates, making them a good option for those with enough equity in their primary residence. Remember, however, that your home serves as collateral, putting it at risk if you default on the loan.

How To Get an Investment Property Loan

Securing an investment property loan involves several steps that require careful planning and consideration.

1. Prepare Your Financial Profile

Lenders will evaluate your application based on your credit score, income and DTI ratio—among other factors. Saving a sizeable down payment can also be helpful. Lenders often require a larger down payment for investment properties than primary residences because of the higher perceived risk.

2. Research Different Loan Options and Lending Institutions

From conventional loans offered by banks to private money loans, understanding the various types available and their respective requirements will ensure you choose the most suitable investment property loan for your needs and circumstances.

3. Consider Economic Factors

Some economic factors, such as decisions made by the Federal Reserve or government policies, are easy to overlook during the planning process. While they’re beyond your control, these factors can greatly impact interest rates and the overall cost of borrowing, so it’s crucial you stay up to date on the news as you shop around for investment property loans.

4. Submit Your Application

Once you take these steps, you can approach lenders with a robust application, improving your chances of securing a loan for your investment property. The process can be complex, so getting advice from a real estate professional or experienced investor can be beneficial.

Find Competitive Mortgage Rates Near You

Compare lenders and rates with Mortgage Research Center

Pros and Cons of Investment Property Loans

Before committing to an investment property loan, consider the pros and cons of taking on this debt.

Pros

- Ability to finance income-producing properties. Investment property loans allow you to finance the purchase of rental properties that generate income. Moreover, the return on investment (ROI) for rental properties is typically higher than other investments.

- Faster approval time. Some types of investment property loans, such as private money loans and hard money loans, can be approved and funded within a few business days.

- Long-term appreciation. Real estate investments can appreciate significantly over the long term, generating a higher ROI.

Cons

- Difficult to qualify for. It can be more difficult to qualify for an investment property loan than a conventional loan due to stricter eligibility requirements imposed by lenders. You may have to provide in-depth financial documents and have a solid credit history to prove your ability to repay the loan.

- Higher interest rates. Because investment properties represent more risk for lenders, they tend to come with higher interest rates than loans for owner-occupied homes and second homes.

- Higher down payment requirements. You may have to put more money down for an investment property loan than a residential mortgage. In some cases, lenders require a minimum of 25% or more.

Pros and Cons of Conventional Loans

Conventional loans, like investment property loans, can be used to invest in real estate—but the features of a conventional loan might make them a better option for you.

Pros

- Wider availability. Conventional loans are more widely available than investment property loans, so you may have a better chance of getting approved or finding an option that’s right for you.

- Lower interest rates and down payment requirements. Because conventional loans tend to come with lower interest rates and down payment requirements than investment property loans, they may be more affordable. For instance, conventional loans, in some cases, require as little as 3% down.

- May be easier to qualify. You don’t need excellent credit to qualify for a conventional loan. This can be beneficial if you don’t meet the strict eligibility requirements of an investment property loan.

Cons

- Limited loan amounts. Because conventional loans are federally regulated, they sometimes have lower maximum loan amounts than investment property loans. This means you may be unable to finance all the funds you need for your investment.

- More intensive underwriting. While overall it’s generally easier to qualify for a conventional loan, even the best mortgage lenders have to follow strict guidelines. You may have a hard time getting approved or experience a lengthier underwriting process if you’re self-employed or are in a unique financial situation.

- Private mortgage insurance (PMI). You’ll need to pay PMI if you put down less than 20% on a conventional loan. This additional cost can eat into how much you can afford to invest.

Investment Property Loans vs. Conventional Loans

Investment property loans and conventional loans can both be used to finance investment properties, but they differ in a few key ways. Here are the main differences to consider if you’re looking at both types of loans:

How To Get the Best Investment Property Rates

It’s crucial to meet specific requirements if you want to obtain favorable rates on an investment property loan. Maintaining a high credit score is essential. Lenders regard borrowers with a credit score of at least 740 as low-risk, which can result in lower interest rates. You may still qualify for a loan if your credit score is lower, but it will likely be at a higher interest rate. A substantial down payment can also help secure a better rate. Investment properties inherently carry more risk for lenders, so lenders often require a larger down payment—typically 20% of the property’s value or more. However, if you can afford to put down even more than the minimum requirement, you might be offered a lower interest rate. Lenders will also consider your DTI ratio, the condition and location of the property and your experience as a property investor.