Original Title: “Coinbase and Glassnode: The Q4 2024 Guide to Crypto Markets”

Author: Coinbase & Glassnode

Compiled by: Felix, PANews

What changes have occurred in the crypto market over the past three months? Bitcoin’s price has generally fluctuated within a range, consolidating between $50,000 and $60,000, with some volatility in between. However, a closer look reveals that significant developments are unfolding behind the scenes.

First, the liquidity and complexity of the crypto market have increased this quarter. Institutional interest in cryptocurrencies remains strong. The net inflow of $5 billion into U.S. Bitcoin spot ETFs indicates that institutions are still participating despite occasional fluctuations. Ethereum’s price has reached an all-time high, reflecting that traditional finance is exploring new ways to interact with digital assets. Meanwhile, stablecoins continue to be one of the most widely used applications in cryptocurrency, with a market capitalization reaching a record $170 billion, and the growing trading volume proves their ongoing utility in cross-border transactions and other areas.

This report will comprehensively cover the forces driving these trends. It also points out potential shifts and directions for major assets (especially Bitcoin and Ethereum) as the year comes to a close.

Here is the full report:

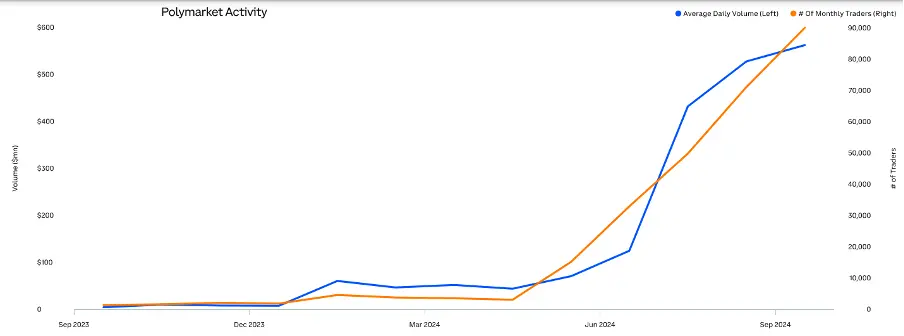

Polymarket is a groundbreaking application for the crypto election year, exemplifying how blockchain technology can enhance market and information transparency, accessibility, and trust.

Data Source: @rchen8, Dune Analytics, Grayscale Investments

Data as of September 30

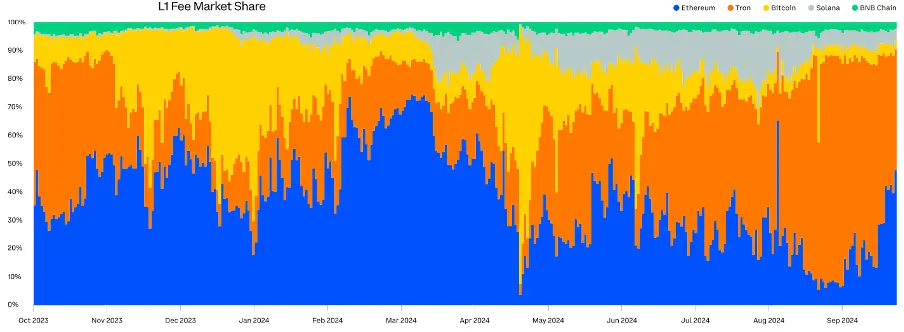

In L1 blockchains, Ethereum’s fee market share has rebounded from a low of 9% at the end of August to 40% at the end of September.

Source: Token Terminal, September 24

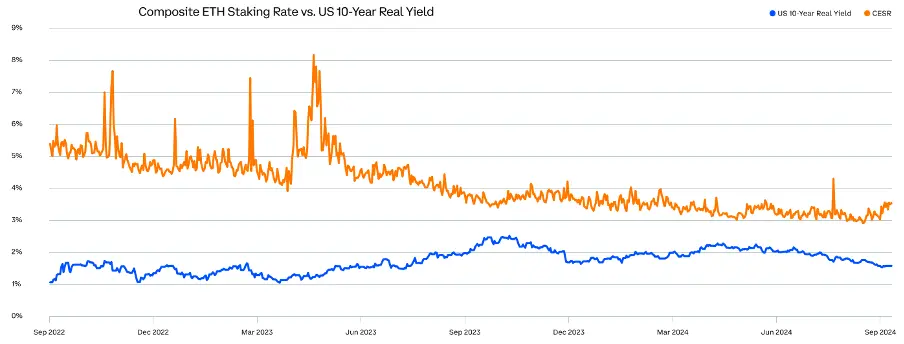

The staking yield for Ethereum is more than twice the real (inflation-adjusted) yield of 10-year U.S. Treasury bonds.

Data Source: CoinDesk Indices

(CESR measures the average annualized yield earned by validators staking ETH, consisting of consensus rewards and priority transaction fees; while ETH’s inflation rate has been negative for most of its history, it has recently turned positive, so stakers should consider its impact on staking yields.)

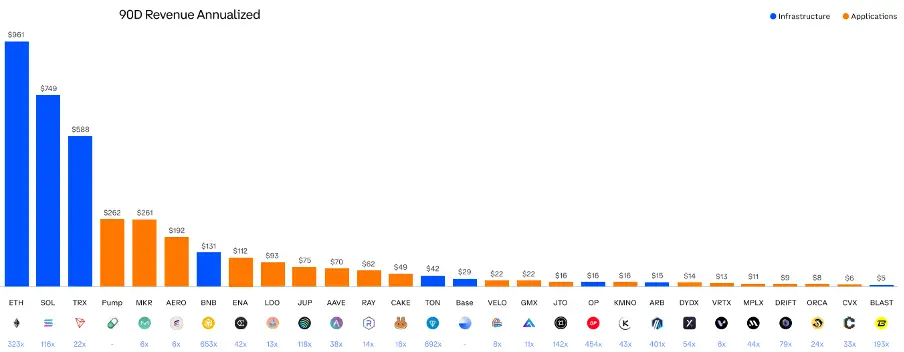

Many successful applications have generated returns that exceed the infrastructure they operate on.

Source: Token Terminal, MakerBurn, DeFiLlama, Tronscan

Annualized revenue calculated over the past 90 days, Solana’s revenue includes base fees, priority fees, and MEV tips; data as of September 25.

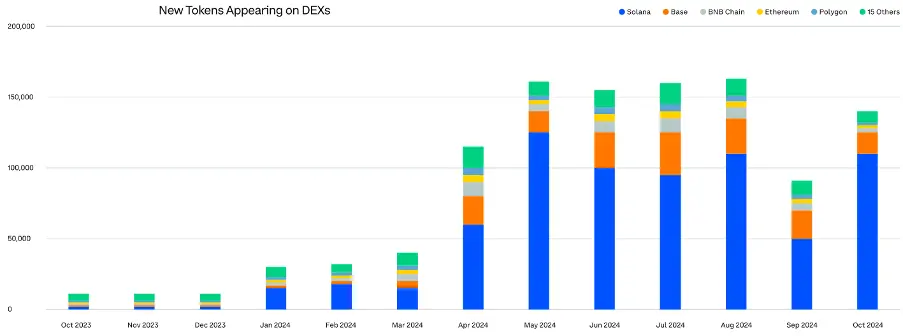

Last year, the number of token issuances surged 13 times, with Solana capturing the largest share.

Source: Dune Analytics

Market Overview

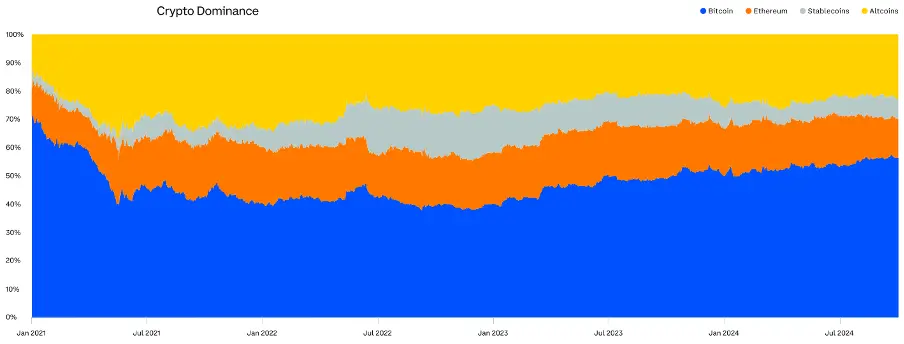

As market participants are attracted to the highest quality assets, the dominance of BTC and stablecoins has increased in the third quarter.

As the market matures, the volatility of BTC and ETH has shown a significant downward trend.

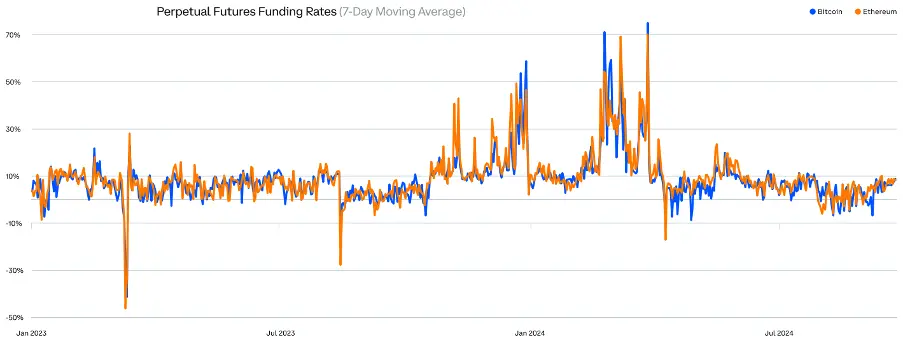

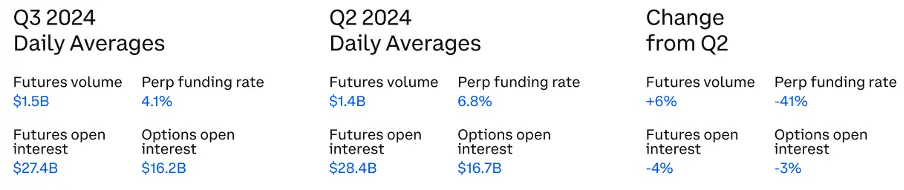

In the third quarter, the perpetual contract funding rates traded within a narrow range, indicating a balance between buyers and sellers in the market.

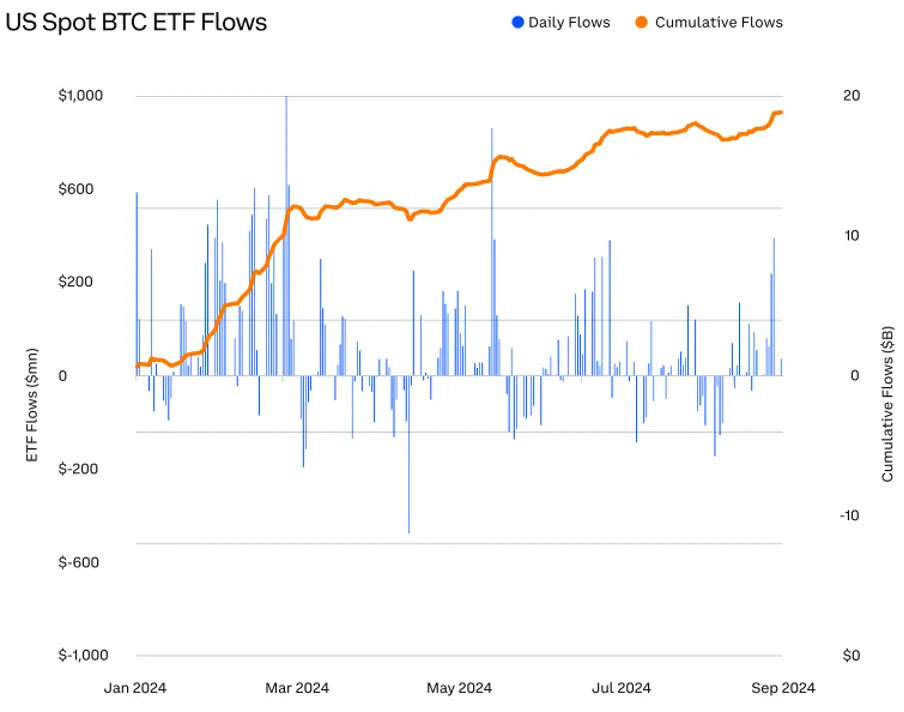

The U.S. spot BTC ETF attracted over $5 billion in net inflows in the third quarter.

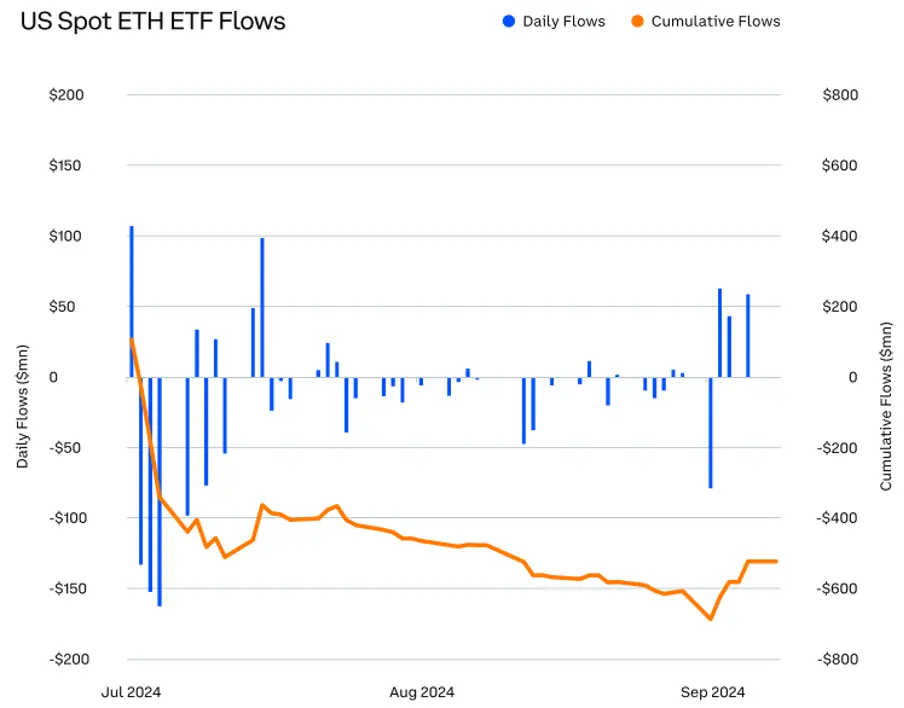

After several weeks of outflows, the U.S. spot ETH ETF saw a rebound in inflows at the end of the third quarter.

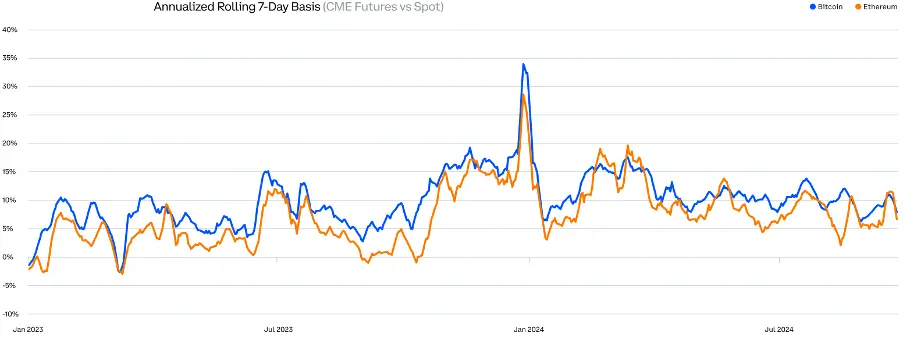

The basis (CME futures minus spot) for BTC and ETH both declined in the third quarter.

Extreme fluctuations in basis, whether positive or negative, are often associated with significant shifts in market sentiment.

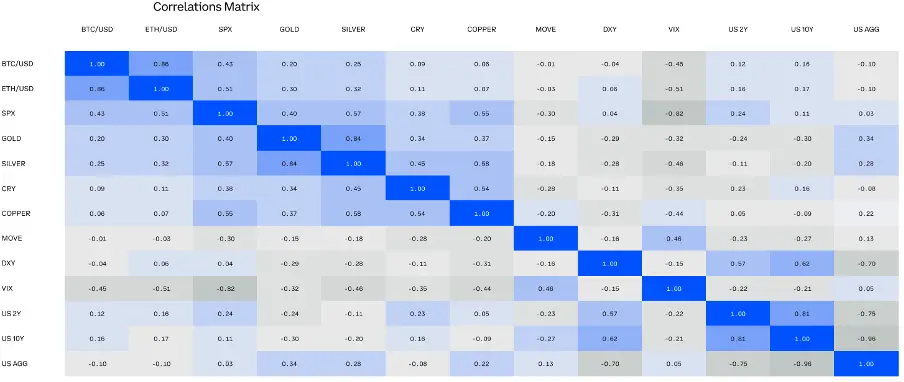

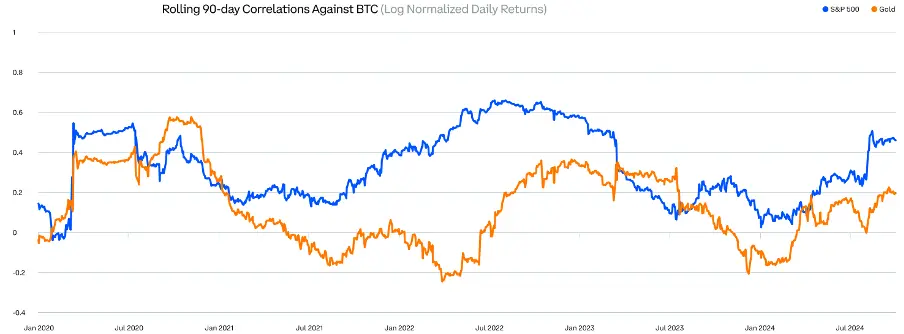

Cryptocurrencies exhibit low or negative correlation with all major asset classes.

Data Source: Bloomberg, Coinbase. Data from July 1 to September 30.

Since 2020, the average correlation of Bitcoin with the S&P 500 index has been only 0.33, and with gold, it has been only 0.13.

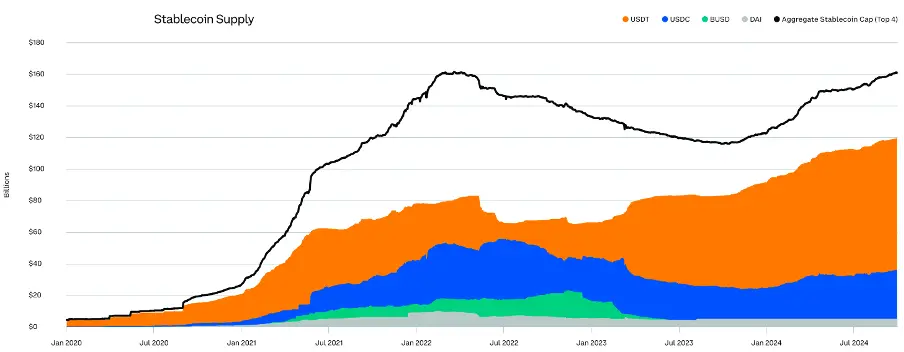

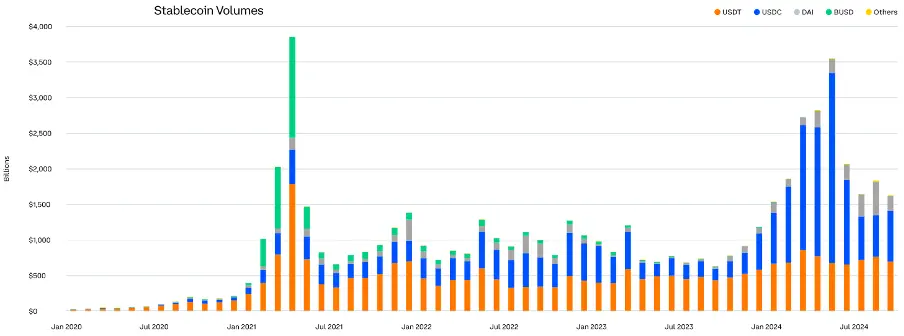

Stablecoin Surge

The total market capitalization of stablecoins reached a historic high of nearly $170 billion in Q3 2024, coinciding with the implementation of new rules by the EU under the Markets in Crypto-Assets (MiCA) regulation.

Both developments reflect the increasing mainstream adoption of stablecoins and the recognition of the advantages they offer, including speed, cost, and security. Stablecoins are increasingly being used to build payment systems, facilitate remittances, and simplify cross-border transactions.

Integrating stablecoins into existing payment systems is just one example of how cryptocurrencies are being applied more frequently in the real economy.

As market participants continue to use stablecoins for various new and existing use cases, the supply of stablecoins reached an all-time high in the third quarter.

Year-to-date, stablecoin trading volume has surged to nearly $20 trillion.

L2

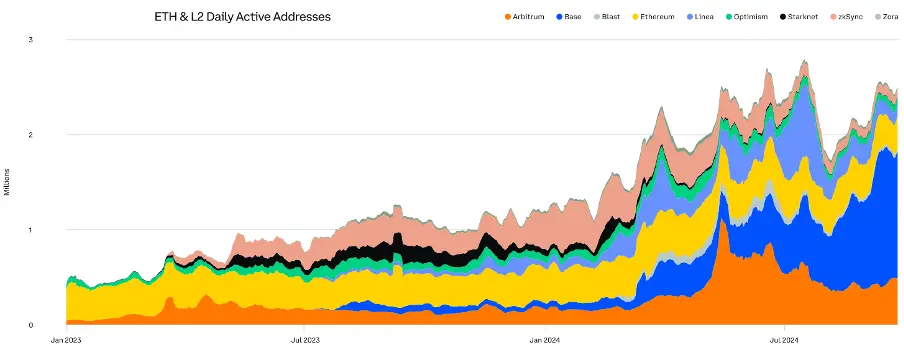

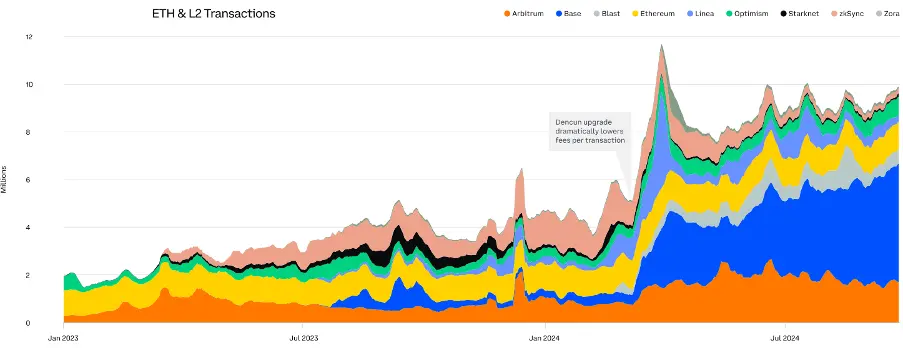

As we enter the fourth quarter, the price of ETH is approaching the levels seen at the beginning of the year. However, beyond the price, there is a rapidly growing Ethereum ecosystem, primarily driven by new innovative L2 solutions.

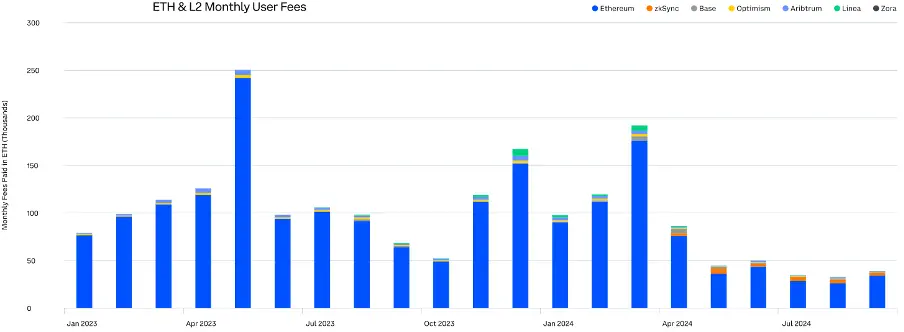

As developers and end-users continue to migrate to the blockchain, both active user numbers and transaction volumes have surged dramatically. Meanwhile, following Ethereum’s Dencun upgrade, fees on L2 have significantly decreased.

While it remains to be seen how activity will develop between Ethereum L1 and various L2s, L2 has brought more users, more activity, and more innovation to the Ethereum world.

This year, the number of daily active addresses in the Ethereum ecosystem has surged dramatically, with L2s showing the most significant increase, with Base leading the way.

With the flourishing of new L2s and use cases, the daily transaction volume in the Ethereum ecosystem has increased fivefold since the beginning of 2023.

After the Dencun upgrade in March 2024, which significantly reduced transaction fees on L2, the total fees paid have dropped significantly despite a surge in transaction activity.

Bitcoin (BTC)

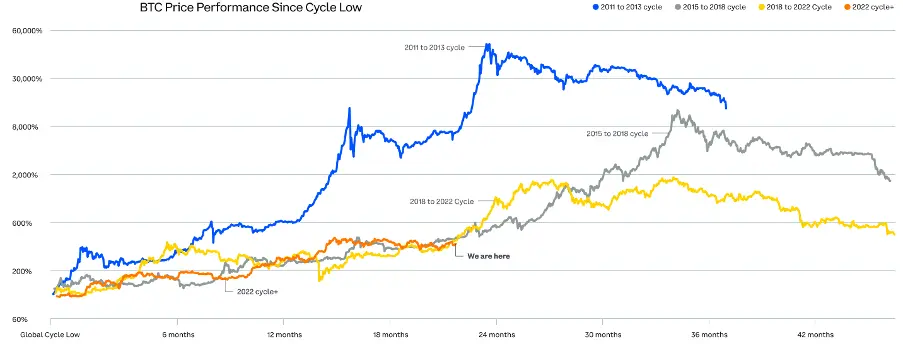

The current BTC cycle is closely related to the cycles of 2015-2018 and 2018-2022, with total returns of nearly 2,000% and 600%, respectively.

Bitcoin has gone through four cycles, each including bull and bear markets. This chart shows how the current market cycle (which began in 2022) compares to previous cycles. (Past performance is not indicative of future results.)

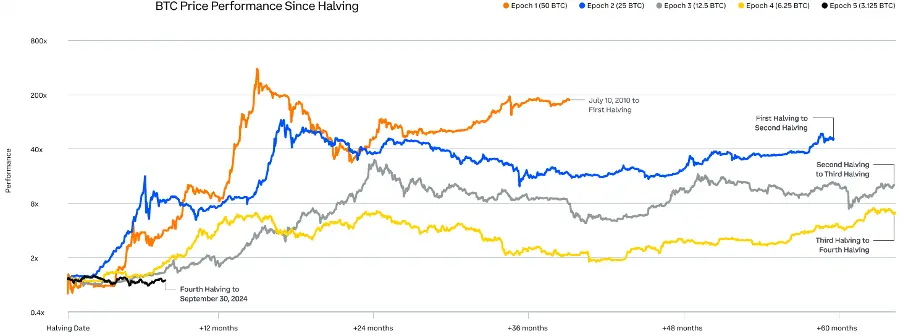

BTC’s performance since the fourth halving has been most similar to that following the third halving, when prices consolidated for several months before rising significantly within a year after the halving.

This chart measures Bitcoin’s total returns during each halving cycle or period. After halvings, prices tend to trade sideways, as seen in the six months since the April 2024 halving. However, in the 12 months following the first three halvings, prices rose significantly. After the first halving, prices increased by over 1,000% in the first 12 months. After the second halving, prices rose by 200% in the first 12 months. After the third halving, prices increased by over 600% in the first 12 months. Since the fourth halving on April 19, 2024 (black line), Bitcoin’s price has decreased by 1.2%.

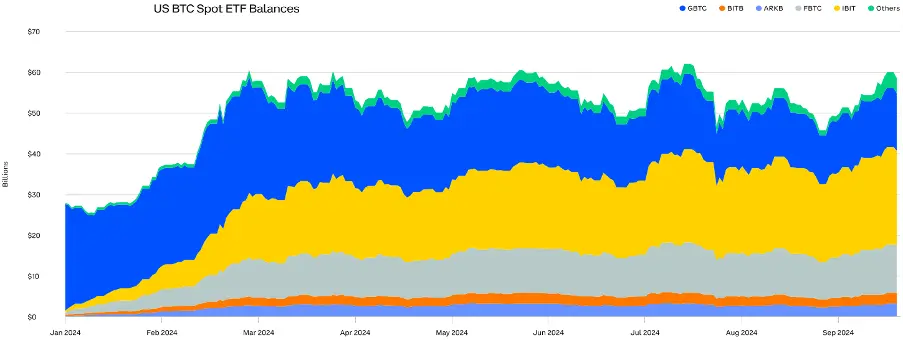

As of the end of the third quarter, the assets under management of the U.S. spot BTC ETF, launched just 9 months ago, have approached $60 billion.

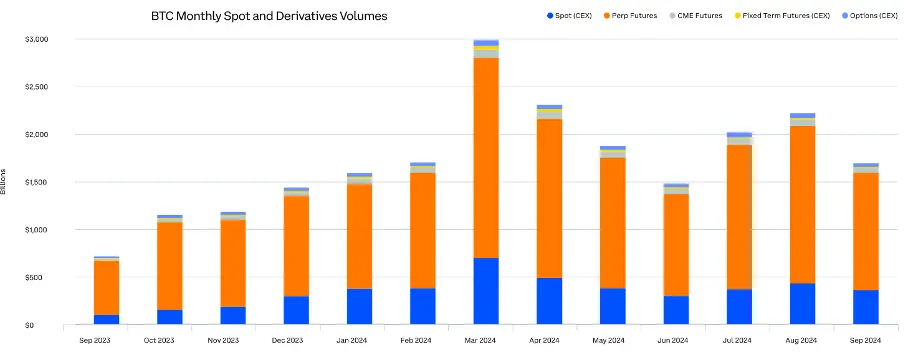

The liquidity in the crypto market is becoming increasingly strong. Year-to-date, BTC trading volume has averaged $2 trillion per month, a 76% increase compared to the same period last year.

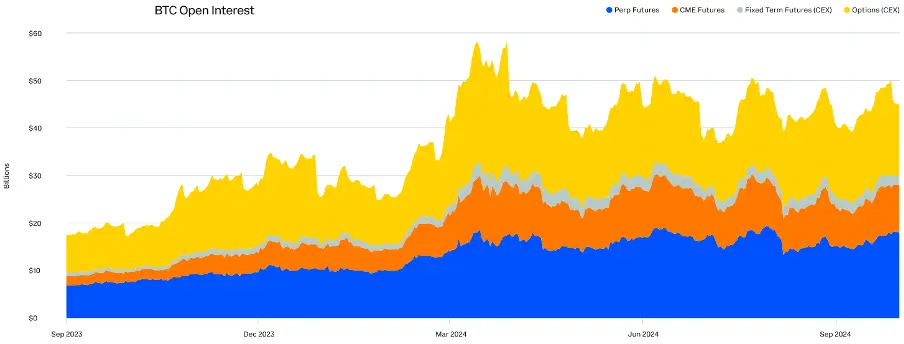

In Q3 2024, the average open interest for Bitcoin derivatives was $44 billion.

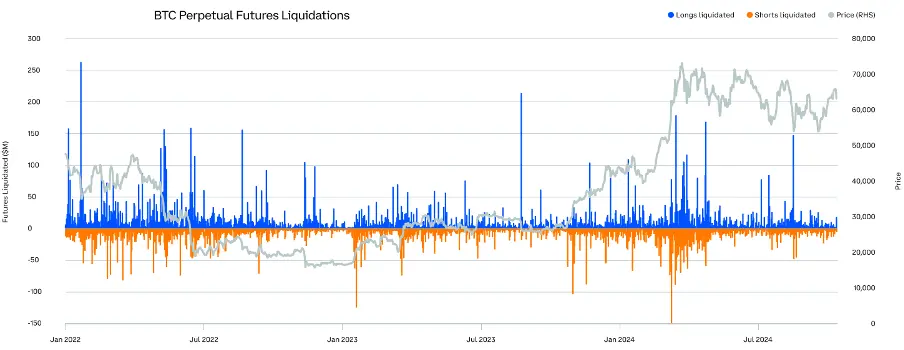

After a significant amount of long liquidations related to yen short arbitrage trades in early August 2024, Bitcoin positions appear clearer.

BTC Derivatives Summary:

BTC Traditional Futures Specifications

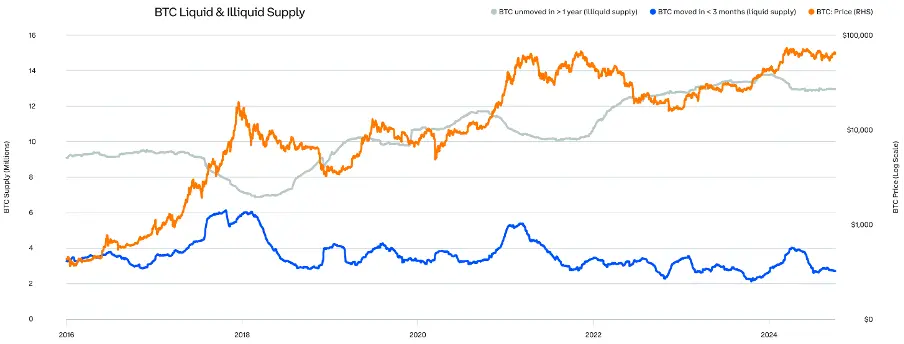

Throughout the third quarter, the scale of BTC’s liquid and illiquid supply remained relatively stable.

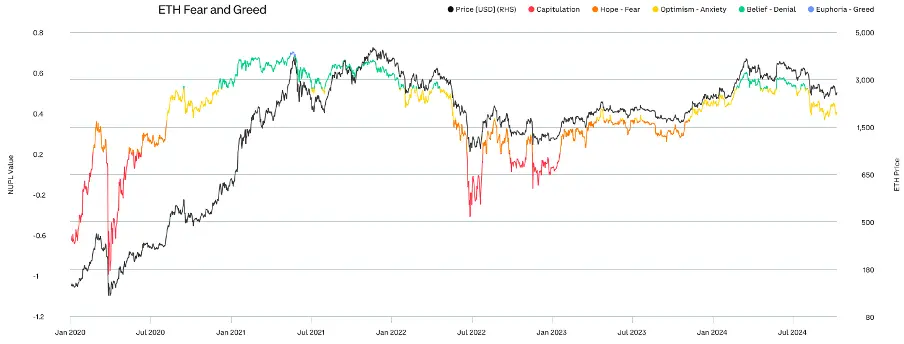

As the market consolidates, market sentiment has shifted from greed to fear, potentially laying the groundwork for the next rebound.

Ethereum (ETH)

After closely tracking the 2018-2022 cycle, the current ETH cycle has begun to show divergence as ETH prices fell in the third quarter.

ETH has gone through two cycles, each including bull and bear markets. This chart shows how the current market cycle (which began in 2022) compares to previous cycles. In the current cycle, ETH has risen over 125% since hitting a cycle low in November 2022. (Past performance is not indicative of future results.)

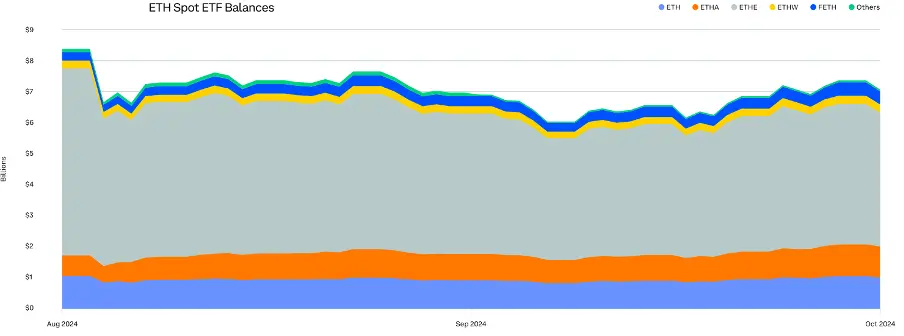

The U.S. spot ETH ETF launched in July, reaching a total size of $7.1 billion by the end of the third quarter.

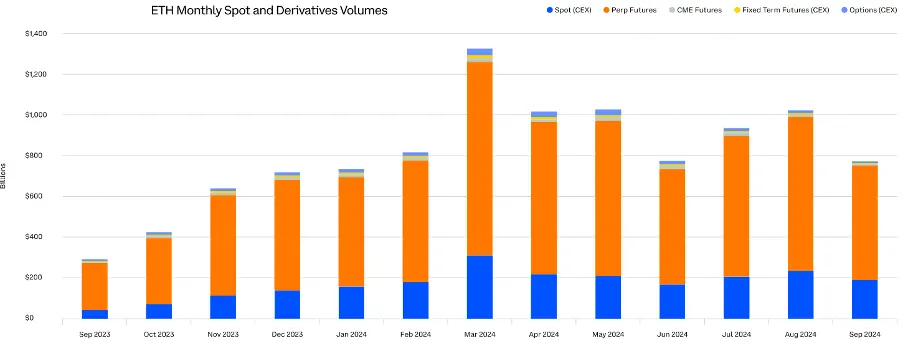

The liquidity in the crypto market is becoming increasingly strong. In 2024, ETH’s average monthly trading volume is $930 billion.

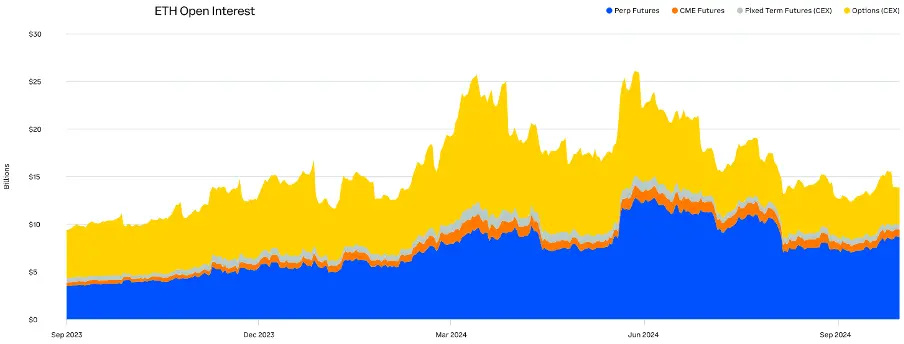

In Q4 2023, the average open interest for ETH derivatives was $15 billion.

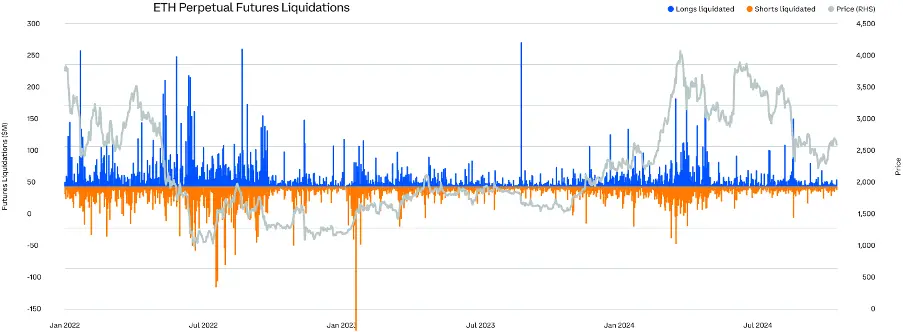

After the launch of the spot ETH ETF in the U.S. and the liquidation of yen short arbitrage trades in early August, the volume of ETH long liquidations surged significantly.

ETH Derivatives Summary

ETH Traditional Futures Specifications

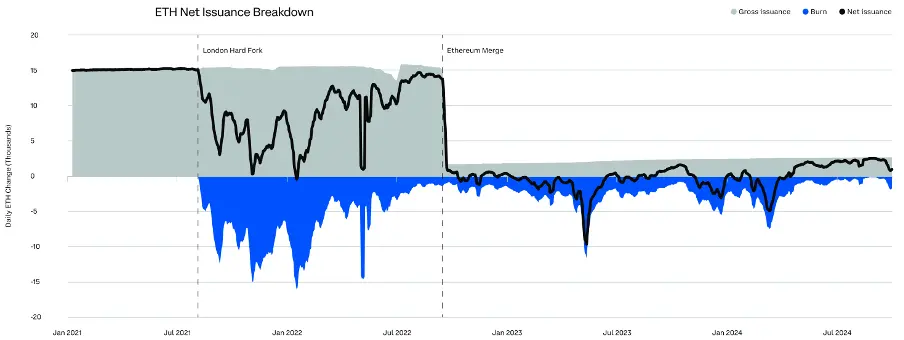

Despite a rise in fees at the end of the third quarter, ETH continues to experience net inflation.

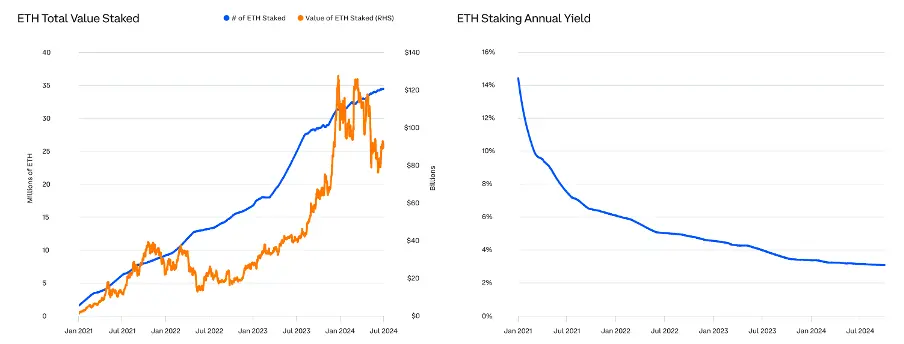

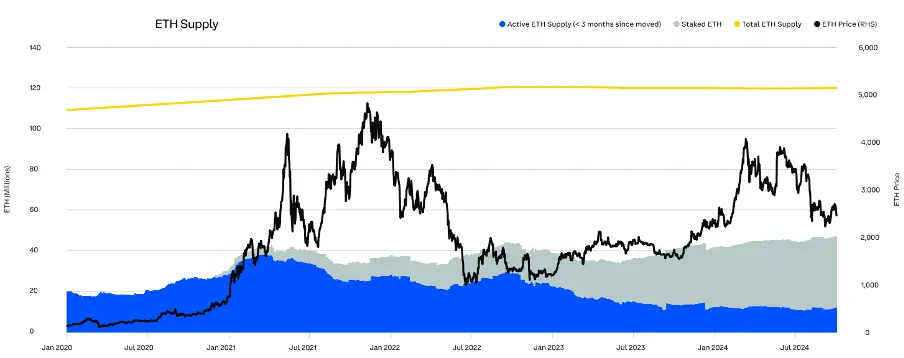

As more holders seek to realize gains from their positions, the amount of ETH staked reached an all-time high in the third quarter.

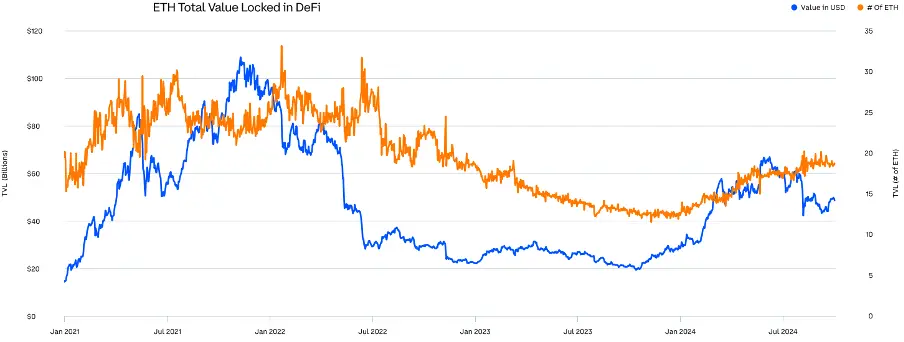

In the third quarter, the amount of ETH locked in DeFi increased by 11%.

Staking has become the primary source of liquidity consumption for ETH.

As ETH prices fell, market sentiment shifted from greed to fear, potentially laying the groundwork for the next rebound.

ChainCatcher reminds readers to view blockchain rationally, enhance risk awareness, and be cautious of various virtual token issuances and speculations. All content on this site is solely market information or related party opinions, and does not constitute any form of investment advice. If you find sensitive information in the content, please click “Report”, and we will handle it promptly.