The reason?

Amazon and Axio are long-time partners. In 2016, the latter partnered with Amazon to offer loans to its merchants and then buyers on the platform. Amazon is also an investor in the company, starting with Series C in 2018. One investor, who didn’t want to be identified, said that the purchase was in the making for six years.

But that’s not the only reason for the lack of drama. The deal was merely a “good outcome” for some investors but not an extraordinary one. The acquisition value is just shy of the $206 million the company raised from investors, including Amazon. The fintech startup has, in fact, seen an erosion in valuation, which insiders link to a slower-than-expected growth of the fintech lending industry. At its peak, Axio was valued at $350 million in 2019.

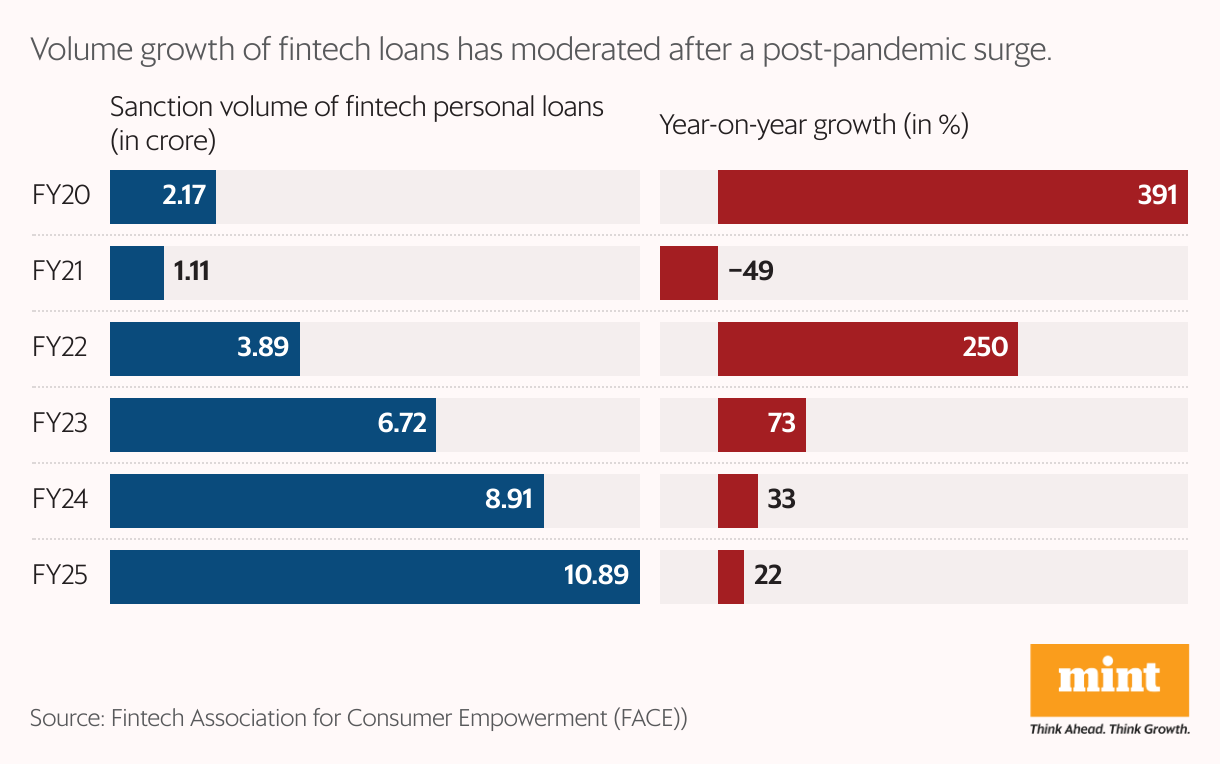

Between 2019 and now, Buy Now Pay Later (BNPL) digital lenders—Axio being one of them—have gone through a rollercoaster ride. Growth has moderated after a post-pandemic surge in numbers.

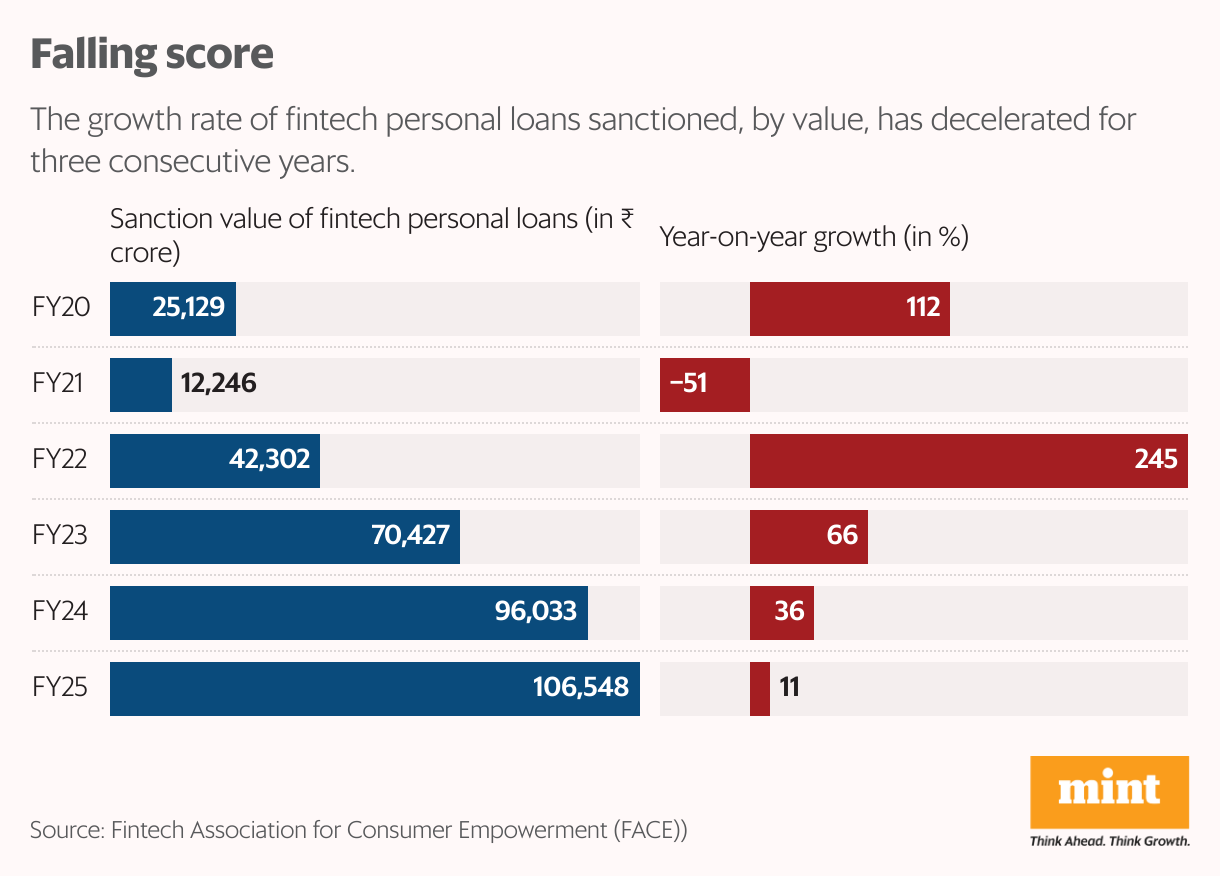

In 2018-19, fintechs sanctioned 4.4 million personal loans, according to the Fintech Association for Consumer Empowerment (FACE), an industry body. While the number has grown to 110 million in 2024-25, the growth rate has decelerated considerably, from a peak of 73% rise in sanction volume in 2022-23 to only 22% last fiscal year. Similarly, there was a sharp deceleration in the value of personal loans sanctioned as well (see chart).

The ‘no drama’ outcome is indicative of these challenges on the ground.

While the market and circumstances are entirely different, BNPL appears to be creating quite a buzz in the West. On 9 September, Swedish BNPL company Klarna, said it had raised $1.37 billion in its US initial public offering (IPO), touted as the largest IPO of the year. It had a market cap of about $18 billion at the close of its listing day.

But larger questions have surfaced in India. Can BNPL make a spectacular revival? How will Amazon gain from Axio now? And can the acquisition boost its fintech ambitions in India?

A short history

Before we answer these questions, let’s look at the Axio story.

The company started life in 2013 as Capital Float, a financing outfit focused on small and medium businesses. It was founded by Stanford MBA class mates Sashank Rishyasringa and Gaurav Hinduja.

Like we mentioned earlier, in 2016, it partnered with Amazon to offer loans to the e-commerce giant’s merchants. However, it soon pivoted to offer credit to customers at the point of sale. In 2020, when Amazon launched its Pay Later offering, it did so through a partnership with Capital Float. This followed Amazon’s participation in the fintech’s funding rounds, starting in 2018. Amazon further invested $20 million into the company in 2024. The startup’s other investors include Lightrock, Elevation Capital, PeakXV Partners, Creation Investments and Ribbit Capital.

View Full Image

Axio today offers two credit products—checkout financing, which allows customers to split the cost of a large purchase over many months, and term loans to salaried and self-employed individuals, similar to the personal loans that banks offer to their customers. In addition, it offers a personal finance management app to help people budget better.

The company, which operates as a non-banking financial company (NBFC), claims to have catered to 10 million customers to date and has ₹2,200 crore as assets under management.

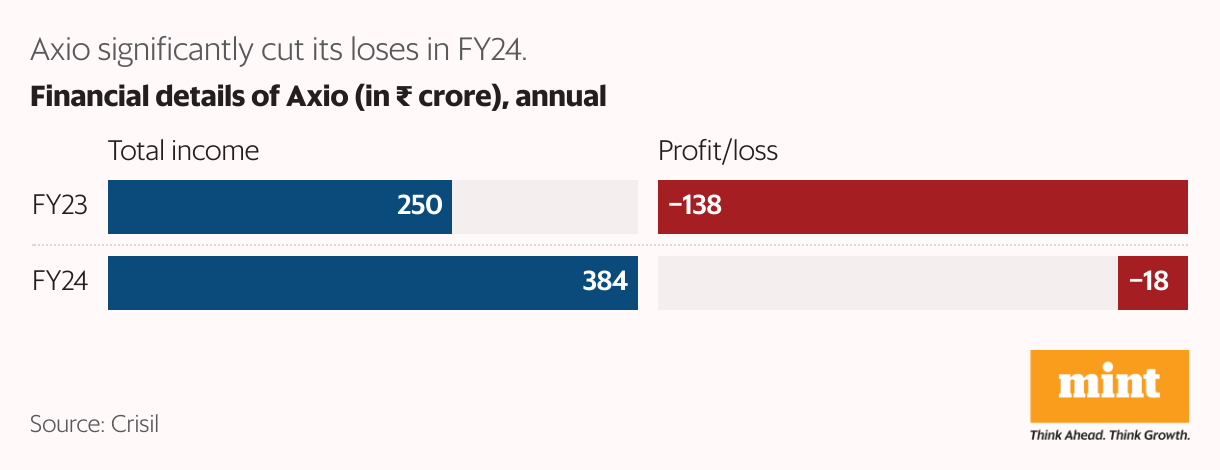

While Axio is yet to turn profitable, it managed to drastically reduce its overall loss by 87% in 2023-24 to ₹18 crore. Simultaneously, it grew revenue by over 50% to ₹384 crore during the year, according to a report from Crisil. On a standalone basis, it reported a pre-provisioning profit of ₹81 crore in 2023-24. This is significant as pre-provisioning profit indicates that the company’s core business operations are profitable before accounting for potential loan losses.

Mahendra Nerurkar, vice president of payments for emerging markets at Amazon, said that the e-tailer was interested in the acquisition considering the potential of the Indian market. “While 10 million is great, when you look at the vast expanse of the Indian consumer landscape, that’s the tip of the iceberg,” he said.

Amazon now hopes to scale Axio’s products. “Not just checkout financing, but also get into other kinds of credit products for consumers, and then beyond consumers into small to medium-sized businesses,” the executive added.

Wild West days

At this point, we need to step back and look at the short history of the BNPL sector as well.

What exactly falls within the ambit of BNPL? Technically, credit cards too are BNPL instruments as are regular consumer durable loans. In the fintech context, unsecured loans offered at the point of checkout online are primarily considered under the BNPL umbrella. Typically, these are smaller ticket size loans, with an average size of ₹9,786, according to FACE.

In the wild west days of Indian e-commerce, circa 2015, the prospect of using the rich consumer data that online retailers had access to, to offer credit to the millions of newly minted online consumers was an exciting one. The launch of India Stack, which simplified know your customer (KYC) norms, the availability of cheap mobile data, and the launch of UPI, also played their part in the popularity spike of all things digital.

Technically, credit cards too are BNPL instruments as are regular consumer durable loans. In the fintech context, unsecured loans offered at the point of checkout online are primarily considered under the BNPL umbrella.

By 2021, the BNPL industry had reached $3 billion to $3.5 billion in size, according to Redseer. At that time, one of the most popular BNPL products was the prepaid instrument or PPI, essentially a digital wallet. What started out as a method for consumers to store their own money digitally in a wallet, was transformed when fintechs started offering PPIs with third-party backed credit lines. These fintechs did not have an NBFC license but acted as middlemen connecting a bank or NBFC with the customer. That was a regulatory grey zone.

“BNPL was a big promise. Every bank was scaling up its BNPL business and everyone was partnering with online retailers. The expectation was BNPL would grow to be a $35 billion market in India by 2030. But, the RBI was extremely concerned with the way they (BNPL lenders) were building their books,” recalled Pratik Shah, managing partner of financial services at EY, a consulting firm.

The bypassing of rules, the rapid growth of consumer debt, the lack of transparency in terms put forward by the BNPL debt providers, rising delinquency rates and shady or coercive recovery practices made the RBI step in.

In 2022, the central bank issued a directive saying that PPIs couldn’t be loaded with credit lines. This, along with a previous order—that only banks, NBFCs and other regulated statutory bodies can engage in lending—came as a blow to the still nascent but growing BNPL sector.

View Full Image

The impact was immediate. ZestMoney, which had been a poster child of India’s BNPL sector, shut down in 2023. At its peak, it had a customer base of 17 million and was enabling ₹400 crore worth of loan disbursals a month. Paytm also wound up its BNPL offering, as did PayU.

That was not all. In November 2023, RBI raised risk weights on consumer loans, including personal loans and bank lending to NBFCs, from 100% to 125%. The higher the risk weights, the more capital a bank will need in order to meet the minimum capital adequacy ratios. It was less attractive for a bank to lend to NBFCs now. In turn, this impacted the lending power of NBFCs.

“In India, everything is sentiment driven and everyone turned their tap down,” said EY’s Shah.

While the regulatory tightening may have impacted market spirits, Axio’s co-founder Rishyasringa countered that the regulations clarified the rules of the game. “We have always taken a regulation-first approach. It has created a level playing field where everyone is governed by the same rules,” said Rishyasringa. “Players like us, who have stuck to a conservative approach, stand to benefit.”

The conservative approach and the respect for regulatory compliance, it appears, helped the company both survive and attract Amazon’s attention.

“Even when we decided to partner and invest (in Axio), we wanted to be aligned with the core values of the company and its founders,” Amazon’s Nerurkar said. “We were not looking for somebody who’s just in a rush to scale, only to realize that we have created a book that we can’t sustain. So having that value alignment was very important for us,” he added.

Amazon Pay and Axio have never offered credit lines on PPI.

View Full Image

Amazon, the fintech co.

For Amazon, the Axio acquisition needs to be viewed from the point of view of the company wanting to be a full-fledged financial services player. It already has an online payment aggregator license and an insurance broking license—Amazon Pay is registered with the Insurance Regulatory and Development Authority of India (Irdai) as a corporate agent.

Through the latest acquisition, Amazon now has an NBFC subsidiary.

The e-tailer already offers multiple payment options to its customers. Among them is a pre-paid wallet, an UPI option, and a co-branded credit card with ICICI Bank. BNPL, now, is expected to help expand its user base, and is particularly important considering its low market share in UPI transactions. PhonePe and Google Pay dominate with almost 80% of the UPI transaction market share by volume as of August 2025, according to the National Payments Corporation of India.

BNPL is useful when targeting those who are not able to access credit easily, especially through credit cards. To be sure, credit card usage in India has seen rapid growth—spending for July amounted to ₹1.93 trillion, registering a month-on-month increase of 5.5%, according to RBI data. Total credit cards in circulation are now at 111.6 million.

However, credit cards, which have more stringent requirements, are typically owned by India’s more affluent class or those with high credit scores.

“We don’t want to only serve the well-served. We want to ensure a balance in our portfolio and have a diversified offering,” said Rishyasringa. “We want a good mix of the salaried and the self-employed, for as you go deeper into the credit pyramid, you encounter far more self-employed people. We want a good geographic mix, and a good mix across demographics,” he added.

BNPL is useful when targeting those who are not able to access credit easily, especially through credit cards. Such cards have more stringent requirements and are typically owned by India’s more affluent class.

Look at this from a different angle. India currently has about 850 million internet users, of which only 20-25% shop online, according to a report by McKinsey. The large base of internet users who are not served by credit overlaps neatly with those who will be the next set of e-commerce consumers.

Similarly, Gen Z is 377 million strong and one in four employees today fall in this age bracket. Gen Z is already driving over $800 billion of consumer spending in the country, according to a BCG report. An EY study showed that a whopping 83% of Gen Zs prefer digital-first financial services.

Targeting these two user groups is critical for Amazon’s immediate and long term growth in India, a key market for the company. Axio’s underwriting and risk management expertise will be in play.

Both Nerurkar and Rishyasringa believe that the combination of Amazon’s vast customer insight and Axio’s lending expertise would ensure success.

“Credit works best when it is integrated with day-to-day commerce, when it is available at the point of need, when it is contextual, when it is mapped to an end use,” Rishyasringa said. “This has been elusive for most lenders in India. By being part of Amazon, we see an unique opportunity to achieve this goal and create a seamless experience where credit is part of the commerce experience.”

Key Takeaways

- Amazon wants to be a full-fledged financial services player.

- Amazon Pay, its digital payments arm, already has an online payment aggregator license and an insurance broking license.

- Now, Amazon has received regulatory approval to complete its acquisition of Axio, a digital lender in the ‘buy now pay later’ segment.

- The e-tailer will now have an NBFC subsidiary.

- Axio’s underwriting and risk management expertise will be in play.

- Coupled with Amazon’s vast customer insight, it could help the entity gain a stronger foothold in the credit market.

- The BNPL segment is expected to help Amazon expand its user base, and is particularly important considering its low market share in UPI transactions.