As 2025 heads into its final stretch, fintech in India finds itself at a defining moment, shaped by shifting regulations, sharper business models and a renewed push for sustainable growth.

Payments banks such as Airtel Payments Bank and Fino have begun moving toward the small finance bank pathway, signalling a shift from narrow digital rails to full-scale banking ambitions. Large payments players like Razorpay, Airpay and Cashfree Payments, having built depth across domestic payments, are widening their canvas — their move into cross-border remittances comes at a time when India’s outward remittance market reached more than $29 Bn annually in FY25.

Wealthtech and digital payments continued to deepen their presence in the everyday financial lives of millions — UPI alone processed more than 14 Bn monthly transactions by late 2025 — but capital flowed more selectively. Funding volumes dipped from the hypergrowth era, prompting fintechs to prioritise profitability, sharper unit economics and more durable revenue streams.

The IPOs of Groww and Pine Labs in 2025 have added further momentum, reflecting public-market confidence in scaled fintech models. Meanwhile, the steady performance of earlier listed players such as Policybazaar and Paytm has kept sentiment buoyant, reinforcing the view that fintech is a category where investors can take long-term positions with confidence. Their trajectory has signalled that the broader financial ecosystem now sees the sector as essential, not experimental.

The year also signalled a structural shift that had been taking shape for some time. New licensing paths, clearer digital lending norms and targeted permissions in payments collectively showed that fintech had moved into the financial mainstream. It was no longer operating at the margins but recognised as core infrastructure. The momentum from regulators, innovation bodies and emerging AI frameworks only underscored how deeply the sector had begun contributing to the economy.

“I saw 2025 as a year when the industry finally came of age. The sector had been evolving for a decade, but this was the year when it demonstrated maturity in a visible and undeniable way. It had impact, scale, and finally, legitimacy,” said Premji Invest’s Bijith Bhaskar, a partner in the India Private Markets team who works closely with the firm’s financial services and fintech portfolio.

As India enters 2026, the sector stands more stable, more accountable and more focussed and the next phase will be shaped not by speed, but by precision and resilience.

“2025 was the year India proved that financial innovation can be both deeply inclusive and globally scalable. With UPI now powering over 80% of all digital payments, it is clear that the next wave of growth will come from new behaviors such as conversational and agentic payments, biometric payments and intelligent cross-border flows,” said Akash Sinha, CEO & cofounder, Cashfree Payments.

So, what opportunities await fintechs in 2026? Let’s take a look.

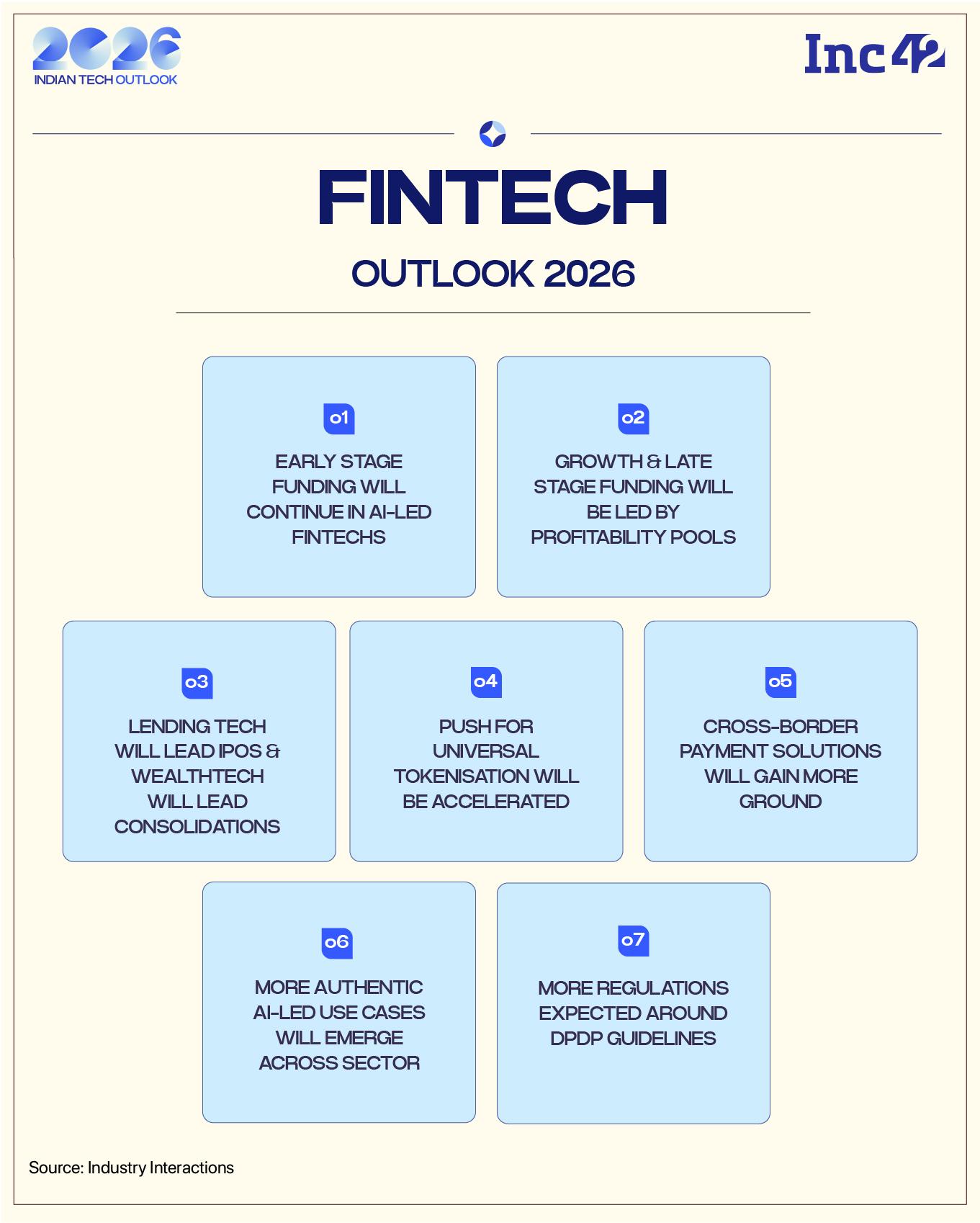

Capital Allocation Will Skew Towards Lending

Early-stage funding will continue in areas such as AI-led fintech because those companies will naturally be young. Growth and late-stage rounds will happen for companies that are pivoting using new-age tools or those operating in established models like lending, where the paths to profitability and profit pools are already visible.

In mature areas such as payments, activity will largely be early-stage since the broader market has already stabilised. The question becomes whether a startup is disrupting something or building a completely new market.

Some of the non-negotiable elements for the investors will be that there has to be a sharp product–market fit and absolute clarity on the problem being solved. The size of the opportunity has to be meaningful, and the profit pool must be visible.

Investors want to know how quickly a company can get to that profit pool because if the business has to list and stand on its own, the path to profitability must be defined. The timeline may vary depending on whether the company is creating a new market or tapping an existing one, but clarity around the profit pools and the point at which the business will reach them is essential.

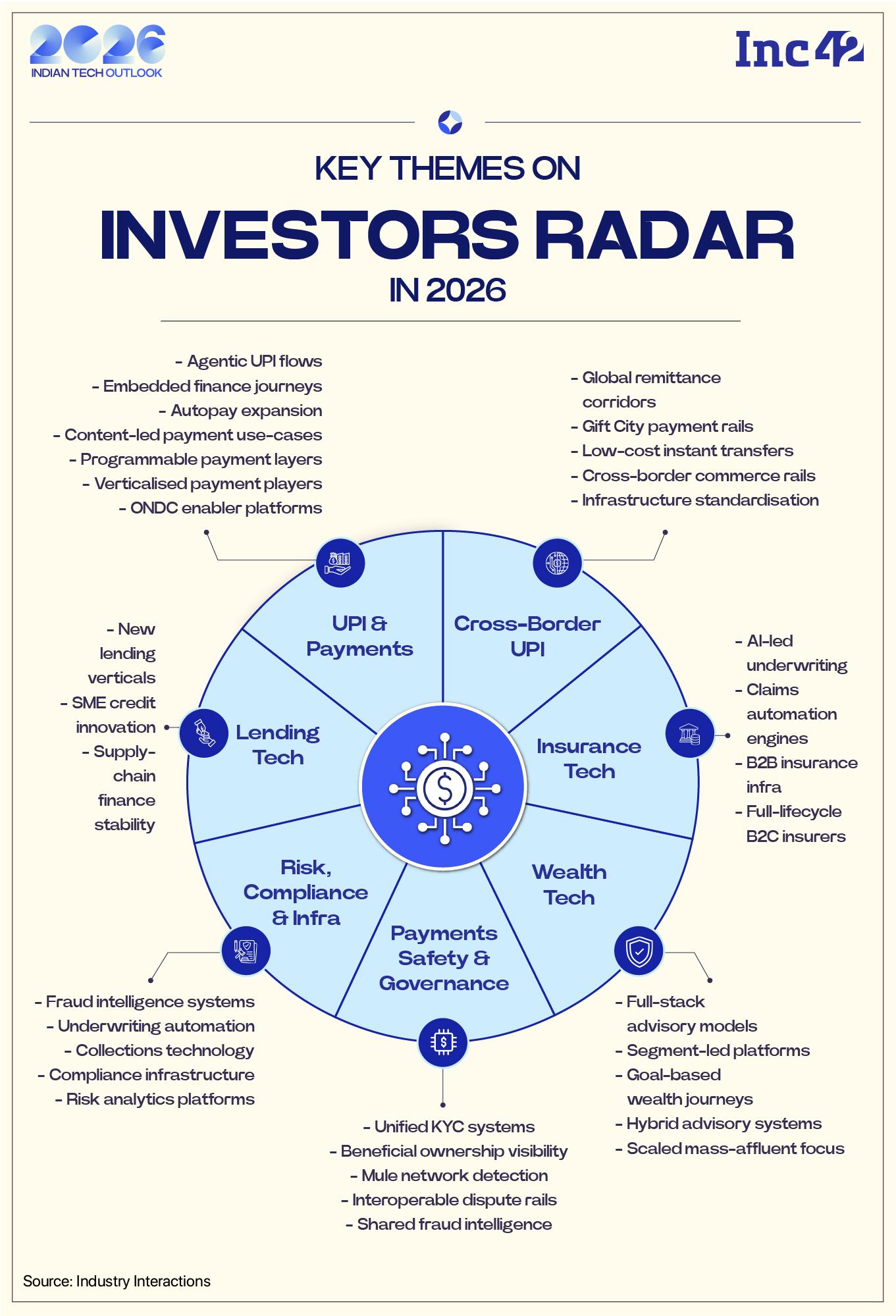

In terms of sectors, the lending side will continue attracting steady capital. Secured segments such as affordable housing and MSME credit should see ongoing interest. Even in consumer lending, entities that run their businesses well and don’t take risks with underwriting will continue to get attention. Consumer lending as part of embedded finance will remain relevant, especially when supported by strong use-case-driven solutions.

Moreover, as Pranay Jain, managing director at Avendus Capital highlighted, credit-on-UPI will create more opportunities for fintechs to partner with banks / fintech companies to own the entire stack.

“The last few years have seen elevated credit costs across the lending segment. That is beginning to show early signs of reversals. The players that have shown resiliency will see disproportionate value creation,” he added

Lending To Lead IPOs; Wealthtech To Lead Consolidation

Analysts expect the IPO pipeline to come from all major areas, but lending will lead. They see several fintech lenders listing over the next few years. Payments will also have a few candidates, and even the insurance space should see some listings over the next two to three years. Lending, however, will show the strongest inclination.

“Indian fintech has been the second largest funding market behind the US, in terms of value and volumes. We expect to see continued acceleration. IPOs: India has seen IPOs in insurance tech and wealthtech, despite a large portion of private funding going into lending tech companies. 2026 could be the year of lending-tech IPOs with the likes of Kreditbee, Fibe and Moneyview looking to hit the markets,” said Avendus Capital’s Jain.

Next, consolidation in payments, insurance and particularly wealth-tech has already progressed meaningfully. As wealthtech platform CashRich founder Sougata Basu highlighted, within wealthtech many smaller players operate today, and some of the larger ones are actively looking to acquire and consolidate.

“Different companies will position themselves differently — some focusing on high-net-worth clients, some on the mass affluent, and some remaining fully digital without segment-specific focus. Consolidation will depend on positioning and on which larger platform wants to expand into a particular segment,” Basu added.

Tokenisation Will Take Its Next Leap

Today, only 40% of users complete the tokenisation process, and nearly 40% of card payment failures happen due to mistyped card details, OTP timeouts, or simply not having the card handy at the time of checkout, resulting in missed revenue for businesses and a subpar shopping experience for customers.

Analysts believe that the fintech ecosystem has immense opportunity to build solutions around this. Earlier this year, players like Razorpay, in partnership with CRED and VISA, launched CardSync, India’s first ecosystem-wide saved card tokenisation solution.

As interest grows around enabling credit for MSMEs and affordable housing, tokenising assets could open new pathways for secured lending. The space is still nascent, but it may evolve into a meaningful growth opportunity as market interest and regulatory direction become clearer.

Razorpay CEO and cofounder Harshil Mathur told Inc42 that as an ecosystem, one needs to move toward a more unified way of verifying users, one that brings together signals from banks, telecom operators, devices, and user behaviour.

This should be supported by stronger protections like universal tokenisation and mandatory linking of devices or SIMs to accounts.

“Fraud monitoring also needs to evolve. Instead of each bank or payment service provider (PSP) working in isolation, we need a shared intelligence network where banks, fintechs, and payment players can securely exchange anonymised (identity-removed) fraud patterns and indicators of suspicious or mule accounts. This collective approach will help the industry detect threats faster and keep users safer,” Mathur added.

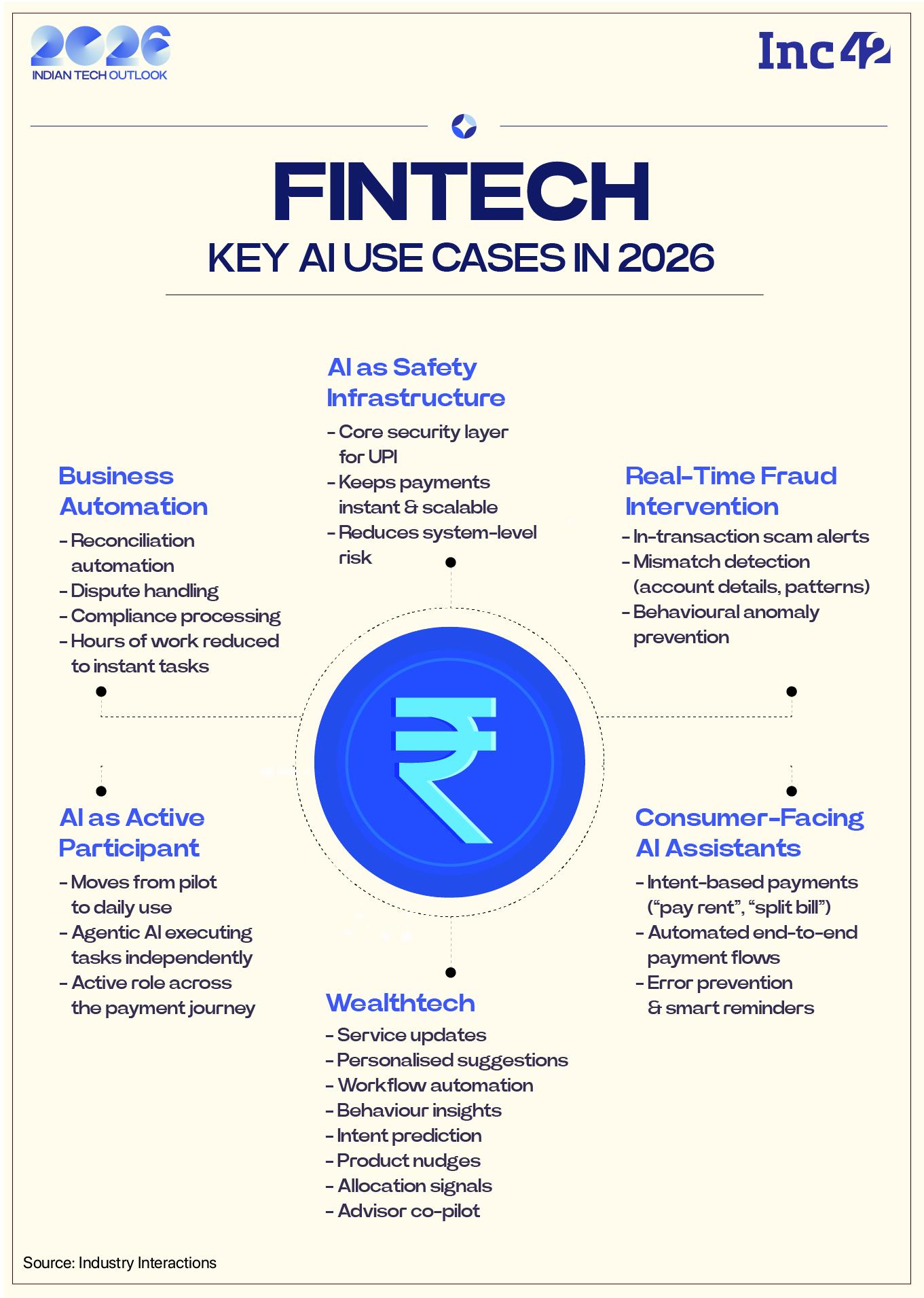

AI-Led Fraud Detection Will Become Mainstream

AI will continue to play a role as an enabler in data analytics, underwriting, fraud prevention, bank statement analysis and more. The analysts sought 2026 as a pivotal moment for fintech infra players where they would see margin compression on products that could get disrupted by AI and newer models to develop that leverage products on top of AI.

Checkout journeys will shrink from multi-step flows to simple intent-led confirmations. But with this scale comes responsibility. Fraud value has tripled this year and the ecosystem must respond with far more agility.

As a result, a major impact of AI will be seen in fraud detection. As the analysts we talked to highlighted, with fraud velocity increasing and dynamic authentication rules kicking in, banks and TPAPs will need continuous, model-driven risk scoring instead of rule-based checks.

“This is why banks are cautious about front-facing AI services, focusing primarily on back-office optimization and efficiency,” said Ramki Gaddipati, APAC CEO and cofounder at Zeta.

What will change in 2026 is not just the adoption of AI, but its integration at the protocol level: shared behavioural signals, device intelligence, telecom data, and mule-account indicators feeding real-time models. As these shared models mature, risk engines will detect anomalies earlier, intervene mid-flow, and personalise friction to users rather than applying blanket controls.

Privacy Regulations Could Change Things

As India builds on its leadership in real-time payments, 2026 will focus on smarter, more secure, and compliant digital transactions.

The Data Protection and Privacy (DPDP) Bill will shape industry priorities as regulators align frameworks with its intent. Analysts expect the RBI to refine expectations, clarifying how data responsibilities are shared and enforced. Gaddipati notes this comes alongside the April 2026 deadline for alternate factor authentication, requiring every digital transaction to include an additional layer beyond OTP.

“This alone will keep payment players occupied, but the implications run deeper. The blurred boundaries between banks and fintech partners will come under strain as contracts are revisited to ensure fiduciary responsibilities are clearly honoured and that banks can rely on partners under well-defined conditions,” the Zeta cofounder added.

The industry will undergo a period of questioning and introspection around its obligations under DPDP as timelines tighten. With expectations now clearer, the RBI may focus on clarifying and reemphasising existing guidelines — particularly around information sharing — rather than drafting new ones. This wave of compliance work will keep the broader ecosystem busy, not just BFSI, although the sector’s complexity means the impact will be felt more sharply there.

The largest gaps remain in connectivity, merchant onboarding, and access to contextual financial tools. Growth in semi-urban and rural markets requires offline-ready payment solutions, simplified onboarding in local languages, and bundled services that combine payments, credit, and bookkeeping. A partnership-driven distribution model will be essential for meaningful penetration.

At the same time, India’s inclusion story must reach far beyond smartphone-native users. Tier III and beyond will leapfrog into formal digital payments through biometric authentication, vernacular conversational interfaces and trust-centred onboarding. The next decade of growth will come not from adding more channels, but from designing them around the language, habits and confidence of everyday users.