One of Pete Townshend’s most famous lines, delivered in one of The Who’s first big hits, My Generation, went: “I hope I die before I get old.”

He didn’t. That’s a good thing given the amount of quality compositions he’s penned over the decades.

But it was a line that became anthemic as post-war youth abandoned the values of their parents during a time of great social and political upheaval, much of it revolving around the war in Vietnam.

It may have taken six decades, close to almost two generations, but suddenly a yawning rift once again is apparent.

While the 60s conflict had its roots in culture, the foundations for the current unrest are wealth and, more specifically, the unequal distribution of it.

As an issue, it’s been bubbling away for most of this century.

Baby boomers (of which your diarist is one) initially were blamed for the degradation of the planet, for caring more about lining their pockets than defending the environment for their offspring.

But, overwhelmingly, it is living standards and the wealth disparity between the generations that now have split society.

Many older Australians merely brush it aside as whingeing from a self-entitled generation. They did it tough too, they argue, and were forced to scrape and save just to get ahead.

But it is not that simple. As our economy has developed and evolved, it has skewed the balance of wealth overwhelmingly towards older generations. It was never planned, but it happened.

And the catalyst for much of the current discontent has been the speed and the extent of the changes in interest rates.

The downside of deregulation

Rates may be the instrument of pain. But it is real estate, and the Australian obsession with owning it, that has marked the battleground.

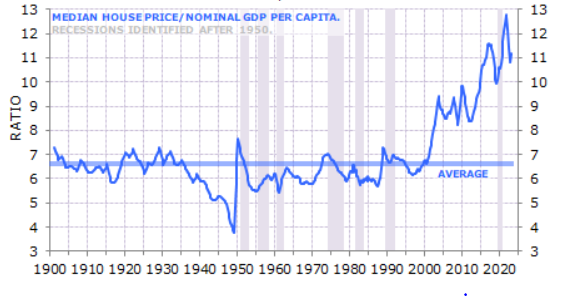

Right up until the late 1990s, wages growth largely kept pace with property. If you want to talk averages, most Australians paid around three times their annual income for a house.

It wasn’t so much that interest rates were restrictive. In many cases, the bank simply couldn’t give you the money you wanted, particularly in the years before deregulation in 1983.

But, as the graph below illustrates, just before the new millennium that relationship between wage growth and real estate prices broke down as our banks discovered a huge pot of cash on offshore wholesale markets and began importing it.

“House prices have boomed since 2000, far outpacing income growth,” economist Gerard Minack says.

“The result is a collapse in affordability and a significant increase in the real cost of housing, either as an owner or renter.”

Younger Australians, particularly those trying to get into the market, now routinely borrow six or seven times their income to land a home.

While it grated as the trend continued, the blow was softened partly as inflation was kept in check and interest rates kept easing, thereby making it easier to service ever-bigger home loans.

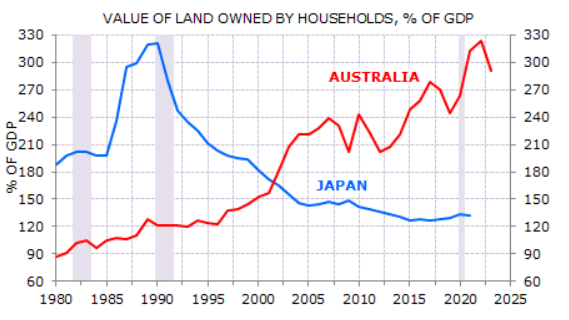

Our housing boom now almost matches Japan’s 1980s bubble, as this graph illustrates, demonstrating just how skewed our economy has become to real estate.

Now that the 30-year decline in interest rates has violently reversed — with 13 rate hikes on the hop, some of which were double hits — those who bought in the past decade and particularly the past four years are furiously paddling just to avoid going under.

Why we’re different

Reserve Bank of Australia deputy governor Andrew Hauser has been startled by the untoward attention.

At an Economic Society of Australia event in Brisbane, he said media attention — a proxy for community attention — on interest rates was more intense than in his homeland, the United Kingdom.

That’s because, unlike the UK, Europe and the US, the vast bulk of our home loans are variable-rate loans. Even our fixed-rate loans are for periods of less than five years.

That means rate hikes have a greater and more immediate impact on household spending in Australia than in any other developed nation.

And it explains why those who bought during or immediately before the pandemic are bearing a disproportionate share of the pain as the RBA attempts to slow the economy.

For those unable to break into the market, a punishing round of rent hikes — the fastest in decades – has severely eaten into spending power.

At the same time, older Australians with huge amounts of equity built up through a decades-long property boom are spending like there is no tomorrow, frustrating the RBA’s efforts to wind back demand.

It is normal for older generations to be savers after a lifetime of work and for younger generations to be borrowers. But our incredible debt-fuelled property boom, which has seen Australian household debt soar to the second-highest in the world at 112 per cent of GDP, has accelerated the trend and accentuated the wealth gap.

Why rate hikes aren’t working the way they should

Something strange happened to our economy around 2016.

For decades, we’d always imported capital because we invested more in Australia than we saved. But once the mining investment boom was complete and cash began rolling into the country, we began racking up current account surpluses.

According to Tim Hext, Pendal’s head of government bond strategies, that turned Australia into a lender to the rest of the world.

Not only that, it allowed our banks to source more cash from locals rather than running offshore to raise cash for home lending.

And, he says, that has a huge impact on how our monetary policy works.

“If more than two-thirds of our borrowings now come from the pockets of other Australians, then raising rates has larger distributional impacts and less aggregate impacts than previous decades,” he argues.

Loading

What he’s saying is that, instead of taking money out of the economy to slow it down, rate hikes now are just shuffling it around, accentuating the pain at one end (millennials) and gains at the other (boomers).

You can see it in global travel, with huge lifts for those over 65 while the young are curtailing travel and everything right across the spending-habit spectrum.

And it partly explains the conundrum Michele Bullock continually bangs on about. Aggregate demand still outstrips supply, she says. That’s why services inflation remains strong and why we have to keep interest rates high.

But in the next breath she admits the economy is barely keeping its head above water.

Interest rates have only been the primary tool for economic management since the late 1980s, when the last big inflation outburst occurred.

But if interest rates have morphed into a tool to redistribute wealth, it may be time to think about adding more weapons to the inflation-fighting manual before we do some serious damage.

Loading…